The $109 Billion Fortress: How Apple’s Services Juggernaut Is Funding the Fight Against Global Antitrust

For the world’s most valuable technology company, the risks are now measured not just in market share points, but in tens of billions of dollars of potential regulatory exposure. This autumn, as Apple celebrated the launch of the iPhone 17 line, a quieter, more existential battle was playing out in the Delhi High Court, where the company fought an Indian antitrust law that could theoretically slap it with a staggering $38 billion penalty based on its global sales.

Yet, reading the latest annual report from Cupertino is to witness a company in complete financial control, even while facing regulatory chaos. While hardware sales stagnated, the company found salvation in its Services division, which surged 14% to a staggering $109.1 billion in fiscal 2025. This spectacular growth engine is funding one of the most aggressive capital return programs in corporate history, masking the slow corrosion of its once-unassailable iPhone dominance and the mounting geopolitical headwinds.

The Golden Goose's Margin

Apple’s revenue growth—a modest 6% increase to $416.1 billion—belies a profound internal shift. The company is now a dual economy: a high-volume, low-margin assembly business constantly battling supply chain pressures, and a high-margin, software-centric tollbooth business that simply prints cash from the App Store, cloud services, and advertising.

The real story lies not in the revenue total, but in the margin structure. In fiscal 2025, the Services division delivered an astonishing gross margin of 75.4%—a figure only slightly offset by "higher costs," as the management noted in their filing. This contrasts sharply with the entire Product ecosystem, where gross margins were nearly halved, landing at a tight 36.8%.

.png)

This massive discrepancy explains why Services revenue growth is now mission-critical. The iPhone, while still the primary driver of top-line sales at nearly $210 billion, saw growth slow to just 4%. Meanwhile, the Wearables, Home, and Accessories category actually contracted 4%, primarily due to "lower net sales of Accessories and Wearables." The future of profitability rests on the App Store’s continued ability to extract high fees globally.

The Geopolitical Drain

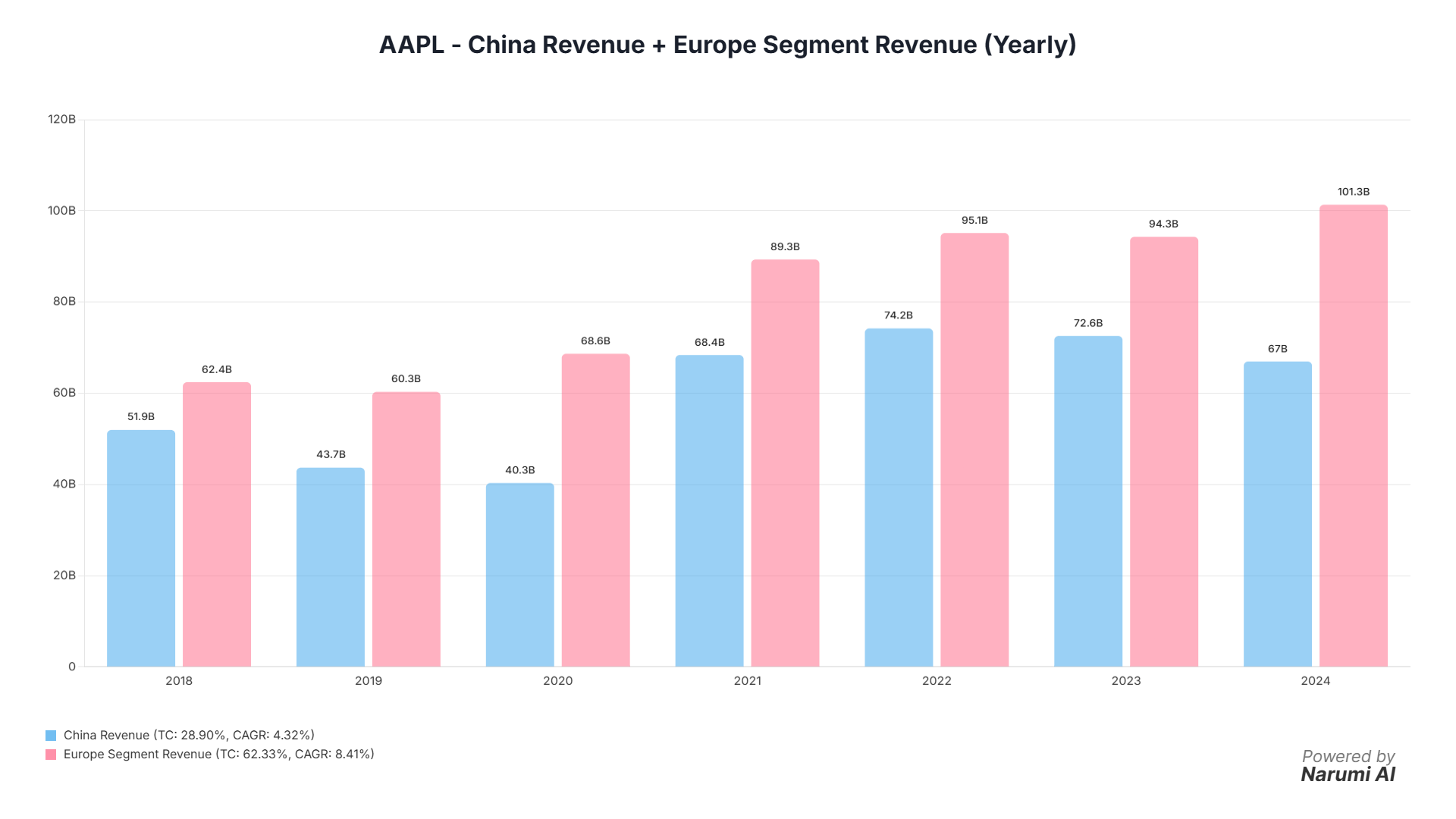

The geographic landscape is becoming increasingly fractured. While Europe emerged as a quiet success story, delivering 10% net sales growth and reaching $111 billion in 2025, the crucial Greater China segment—long seen as Apple’s next trillion-dollar prize—is shrinking.

China net sales dropped 4% in 2025, compounding an 8% drop the year prior, pushing annual revenue down to $64.3 billion. This retreat coincided with the company’s acknowledgement that international trade restrictions, including new U.S. tariffs announced in the second quarter of 2025 on imports from several Asian countries, are impacting the bottom line. Management noted that the decrease in Product gross margin percentage was due, in part, to "tariff costs."

As the company attempts to diversify its supply chain away from China, it faces fresh risks. The filing warns that new tariffs could increase costs and necessitate changes to suppliers, reducing direct control over production and distribution, which could adversely affect cost, quality, quantity, or flexibility to adapt to changing conditions.

The Regulatory Gauntlet

The regulatory threats are not theoretical; they are operational. After facing a EUR500 million fine from the European Commission for noncompliance with the Digital Markets Act (DMA), Apple is now engaged in a pitched battle against regulators in three continents. The Delhi High Court challenge focuses on a statute that Apple argues is "manifestly arbitrary, unconstitutional, grossly disproportionate, unjust" for basing penalties on global turnover rather than just local revenue.

Simultaneously, the company is fighting the U.S. Department of Justice antitrust lawsuit and wrestling with the consequences of the Epic Games ruling, which found Apple in violation of California’s unfair competition law. The court has already referred the company for potential criminal contempt proceedings after finding it in violation of an injunction in April 2025.

To fight this war on all fronts and stimulate future growth, Apple’s investment in R&D has soared, reaching $34.5 billion in 2025, a 10% jump year-over-year, driven by "increases in headcount-related expenses and infrastructure-related costs." This spending, dedicated to everything from the new visionOS software to future AI capabilities, is the cost of staying ahead in a world where, as management warns,

Many competitors primarily employ aggressive pricing, very low cost structures, product imitation, and infringement on intellectual property.

The Denominator Game

Ultimately, the shareholder story remains focused on financial engineering. Even with stagnating product sales and escalating legal costs, Diluted Earnings Per Share (EPS) jumped from $6.08 in 2024 to $7.46 in 2025. This exceptional leap was largely achieved by reducing the diluted share count from 15.4 billion to 15 billion, facilitated by an $89.3 billion share repurchase spree in 2025.

Chief Financial Officer Kevan Parekh and CEO Timothy D. Cook, both signatories on the filing, have maintained the delicate balance: using the high-margin Services cash flow to execute a massive capital return program that stabilizes the stock price, fulfilling the market’s expectation of "continued cash dividends at current or growing levels, and the full consummation of its share repurchase program."

For now, the Services engine is powerful enough to absorb the global shocks. But as the regulatory noose tightens around the App Store—the source of that glorious 75% margin—the market must soon ask whether the company can innovate fast enough to justify its valuation, or if its fate relies solely on shrinking the denominator.

If you want to dive deeper into these numbers, check out our Charting Tools And Other Features to build your own dashboard."