Oracle the “Database Dinosaur” Just Devoured a Data Center — And Its Negative Cash Flow Could Be a Surprising Bull Signal

Oracle, the “Database Dinosaur” Just Swallowed a Data Center

Forget the image of Oracle as that stodgy old database company your parents used. That narrative is dead. This stock matters right now because Oracle, under Larry Ellison’s command, is making an aggressive, high-stakes bet on the future of AI and cloud infrastructure (OCI). The market often misreads $ORCL because its financial statements look messy during this pivot. We are seeing classic signs of a legacy titan transitioning into a hyper-growth infrastructure builder—and the cost of that build-out is massive. But if you dig into the segment data, specifically the revenue velocity of their cloud offerings, it becomes clear that this is a calculated risk, not a slow decline. The key is understanding that the recent financial volatility isn’t a flaw; it’s the cost of admission to the AI gold rush.

The Margin Expansion Story That Hides A Massive Infrastructure Build

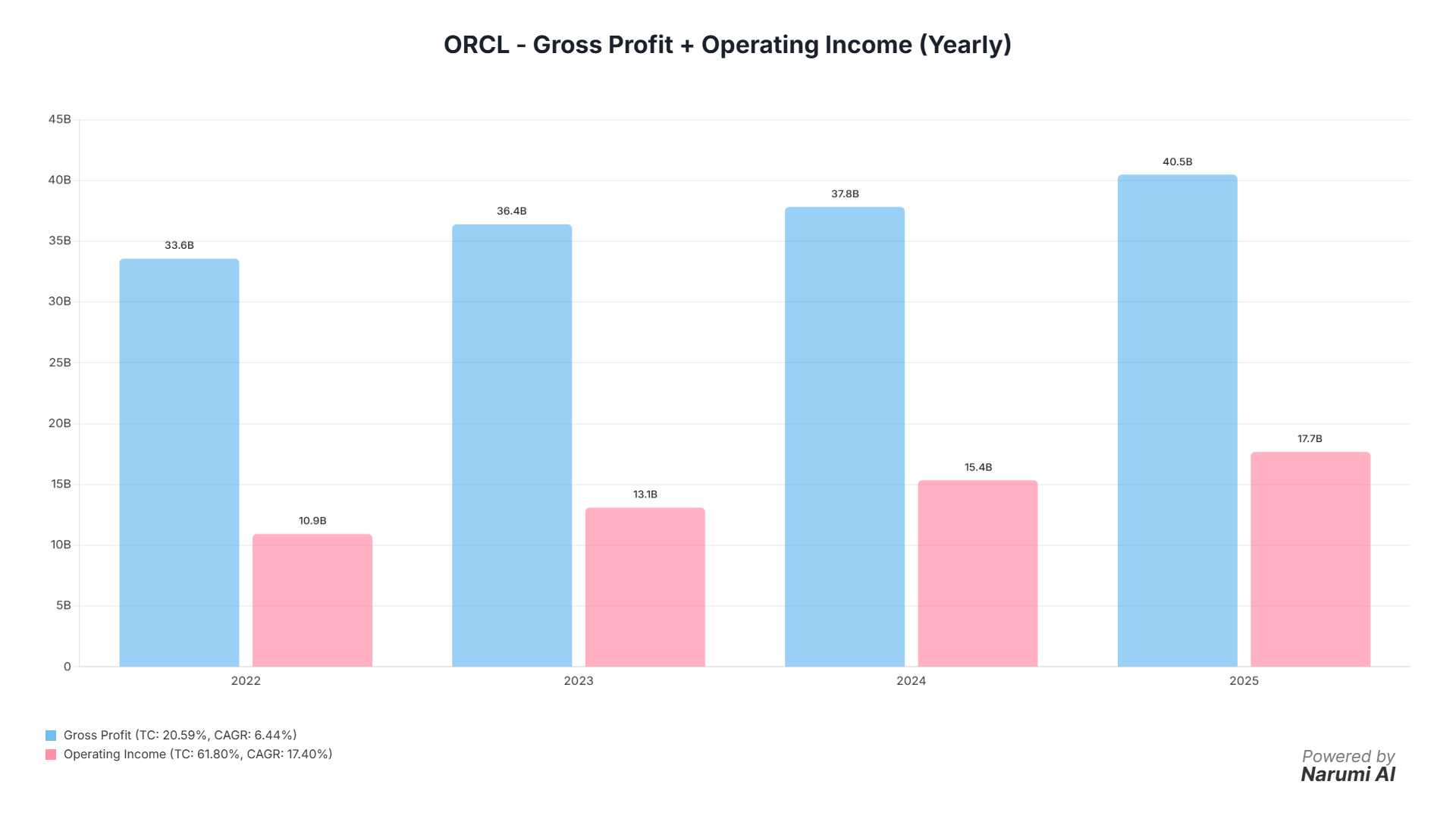

Let’s hit the financials. Revenue is cruising, moving from $49.95 billion in 2023 to $57.39 billion in 2025. That’s solid growth for a company this size. However, the first thing that jumps out is the profitability profile. Gross Margin is actually ticking down slightly, from 72.8% in 2023 to 70.5% in 2025. You might scratch your head and think, 'Wait, where is the efficiency?'

But here’s the smart analyst move: look deeper at the operating efficiency. Operating Income surged from $13.09 billion (26.2% margin) in 2023 to $17.68 billion (30.8% margin) in 2025. The Operating Margin expansion is incredible. This means that while the cost of delivering the new cloud services (Cost of Revenue) is increasing, Oracle is gaining massive leverage on its operating expenses (R&D and SG&A). They are scaling efficiently, offsetting the increased cost of building out server farms.

Now, for the big headline number that probably scared the mainstream news: Free Cash Flow (FCF). FCF went from a healthy $11.81 billion in 2024 straight down to -$0.39 billion in 2025. Yikes, right? But look at the Capital Expenditures (CAPEX). In 2024, CAPEX was $6.87 billion. In 2025, it spiked to a massive $21.22 billion. They aren't losing money; they are spending it furiously to build physical assets (Net Property Plant And Equipment jumps from $21.54 billion to $43.52 billion between 2024 and 2025). This explains the negative FCF. Oracle is effectively saying:

We are dumping every available dollar into OCI infrastructure to capture the AI demand wave.

This shift is also why the massive share buybacks we saw earlier (2022: $16.25 billion) have nearly vanished (2024: $1.20 billion). Capital allocation changed overnight from shareholder return to infrastructure urgency.

Cloud Services Revenue: The Only Metric That Matters Now

If you want the real story, ignore the legacy noise and focus on the segment data. Oracle’s future lives and dies by its Cloud Services Revenue, which is the purest measure of their OCI and AI adoption success. The growth here is accelerating and shows serious momentum.

Let’s look quarterly. Cloud Services Revenue moved from $5.62 billion in Q1 2024 to $7.19 billion in Q1 2025. That’s nearly 28% year-over-year growth in the core engine. Sequentially, the momentum is undeniable: Q4 2024 hit $6.74 billion, and Q1 2025 pushed past that to $7.19 billion. This isn’t just slow, steady enterprise growth; this is the velocity required to compete with the hyperscalers.

Contrast this with the old guard: Hardware Business Revenue. That segment is shrinking, as expected, dipping from $3.27 billion in 2023 to $2.94 billion in 2025. This is the perfect picture of the transition: the legacy business is running down while the new cloud core is firing on all cylinders.

Within the Cloud Services segment, the Infrastructure Cloud Services and License Support Revenue is particularly critical, hitting $7.19 billion in Q1 2025. This is where the AI training workloads land, and it directly justifies that huge CAPEX spike. Oracle is capitalizing on the fact that its competitors are capacity-constrained, building out massive data centers to grab that overflow demand.

.png)

The Devil's Advocate: Are They Biting Off More Than They Can Chew?

Q: Oracle’s FCF is negative in 2025 due to massive CAPEX. Can they sustain this level of spending without diluting shareholders or taking on too much debt?

A: The CAPEX spike to $21.22 billion in 2025 is certainly aggressive, but it’s a strategic choice. They dramatically scaled back shareholder capital returns (buybacks dropped from over $16 billion to $1.2 billion) and shifted that capital directly into infrastructure build-out. They are prioritizing market capture over short-term FCF optics. The market is rewarding them for this high-growth mindset, recognizing the long-term annuity stream these data centers will generate.

Q: Operating Margin is up, but Gross Margin is dipping. Doesn’t that suggest the new cloud revenue is less profitable than the old license support business?

A: Yes, building and running physical cloud infrastructure (OCI) is inherently more expensive than maintaining a traditional database license business. This explains the dip in Gross Margin (72.8% to 70.5%). However, the fact that Operating Margin is simultaneously soaring (26.2% to 30.8%) is the key rebuttal. It proves that the massive scale they are achieving in cloud is allowing them to leverage R&D and SG&A costs far more effectively than ever before. The efficiency gains below the gross profit line are overwhelming the higher COGS.

Q: Revenue growth is strong, but is it diversified? Isn't this just a U.S. story?

A: Absolutely not. While the Americas segment is the largest and fastest-growing—Revenue in the Americas grew from $31.23 billion in 2023 to $36.34 billion in 2025—the growth is global. Revenue in EMEA is also robust, climbing from $12.11 billion to $14.03 billion over the same period. The cloud transition is hitting all major regions simultaneously, confirming this isn't a regional fad but a global enterprise shift.

The Final Word

Oracle is no longer a sleepy database incumbent. It is a high-conviction, high-CAPEX bet on future cloud annuity revenue powered by AI demand. The massive investment in OCI, evidenced by the $21.22 billion CAPEX in 2025 and the resulting negative FCF, is the single most important data point. This is a company betting its balance sheet on growth, and the segment data confirms the bet is starting to pay off with accelerating Cloud Services Revenue. If you believe the AI infrastructure boom has legs, ORCL is positioned to profit significantly from this pivot. This is a solid Hold bordering on a Cautious Buy for investors comfortable with short-term FCF volatility in exchange for long-term cloud dominance.

If you want to play around with these metrics yourself, check out our Interactive Charting Tool to build your own dashboard.